FinS 🍲 for the Soul (13 Oct 2021): mCBDC Bridge prototype enables cheaper and safer cross-border payments

FinS 🍲 for the Soul (13 Oct 2021): mCBDC Bridge prototype enables cheaper and safer cross-border payments

Thanks for to FinS Soup for the Soul. I do a weekly analysis of the latest technological innovation, markets, and regulatory headlines within the financial services industry. If you’re enjoying the read, feel free to subscribe by clicking below. Thanks for stopping by!

Latest headline:

The mCBDC Bridge prototype enables cheaper and safer cross-border payments

Background:

A prototype of Multiple Central Bank Digital Currencies (mCBDCs) has been developed by the Bank for International Settlements and four central banks under the mBridge project. This prototype demonstrates the potential of using digital currencies and distributed ledger technology (DLT) for cheaper and safer cross-border payments and settlements.

The mBridge project is a cooperation between the BIS Innovation Hub Hong Kong Centre, the Hong Kong Monetary Authority; the Bank of Thailand; the Digital Currency Institute of the People's Bank of China; and the Central Bank of the United Arab Emirates.

The prototype reduced the time taken international transfers from a few days to seconds. The system can also operate on a 24/7 basis and halve the transaction costs.

The project will move into the next stage where it will test the platform with stock exchanges in Hong Kong and Bangkok and thirty banks in the four jurisdictions.

Maintaining the stability and credibility of the sovereign.

The foray of Facebook into digital currencies in 2019 with its Libra “global stablecoin” project threatened to crowd out fiat currencies and push central banks into irrelevance. While bitcoin was too small to pose a monetary issue, the encroaching of bigtech into the realm of currency creation amplified the risk of private sector-led disruption.

It opened the possibility of replacing a currency based on political borders with one based on the usage of a private network. This spurred central banks around the world to develop numerous CBDC projects to keep central bank money at the core of the system.

In my previous article, I wrote about the nuanced design considerations in the creation of CBDCs. A further progression of the CBDC is the creation of the mCBDC, which involves an additional layer of complexity—mainly in accommodating domestic mandates and public policy objectives within a shared platform. This mCBDC requires the consideration of governance issues concerning the ability to do monetary policy, control laundering, and apply sanctions when necessary.

CBDCs serve as a tool for central banks to strengthen their monetary sovereignty in the digital age. Central bankers are not directly elected by citizens, but rather are appointed by an elected head of state. Nonetheless, protecting the central bank’s right to issue money is seen as being synonymous with preserving the legitimacy of the democratic bodies voted in by citizens.

Interoperability via linkages or integration.

Interoperability is an essential consideration in the design of mCBDC. It will allow mCBDCs to interact with each other, exchange funds and information, and aid transaction monitoring.

For example, existing point-of-sale terminals need to be connected to digital platforms. Online and offline realms need to be combined to enable digital payments to be made over point-to-point channels, even when users are temporarily offline and unable to connect to payment intermediaries or the internet. Fintech capabilities should be folded into the development of mCBDCs.

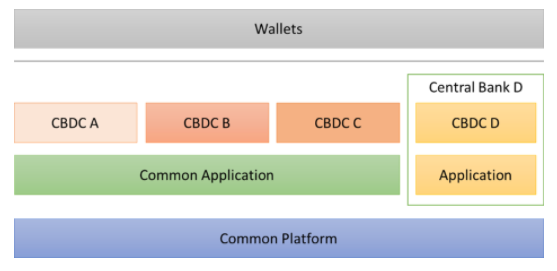

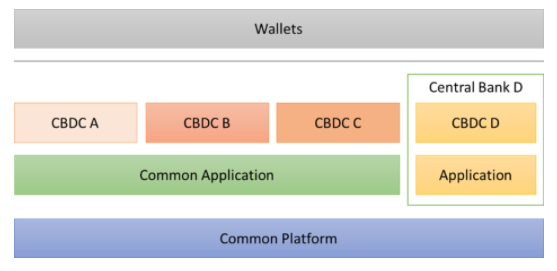

Interoperability within the mCBDC model can be enabled either by merely interlinking separate systems (via technical interfaces or a common clearing mechanism) or opting for deeper integration by establishing a single mCBDC system.

In interlinking separate systems, domestic CBDC systems exist independently and bilateral contractual and operational arrangements are required between central banks for cross-border payments. Such a model may be difficult to scale—for about 200 central banks worldwide, 20,000 bilateral linkages will be required!

On the other hand, a single mCBDC system will operate with a single rulebook, set of participation requirements, and supporting infrastructure. The common platform would likely allow efficiency gains to be reaped. The transactional efficiencies achieved in the mBridge project described earlier is a case in point. However, governance issues around ownership, operations, and control of the shared platform may pose a challenge.

In response to this issue, the Monetary Authority of Singapore (MAS) has proposed unbundling the technology stack to offer segregated and granular levels of controls at individuals layers of the stack. This would allow multiple independent parties to operate their node and even develop their applications within the common tech stack.

How to incorporate bigtech into the model.

Cloud services provide the flexibility to allocate permissions within a layered technical architecture with identity and access management capabilities. The solution provider sets up and manages the lower layers of the technology stack associated with the operating system, networking, computing, security, and backup management. This allows central banks to focus on managing the data and applications on the upper layers of the stack.

Segregated and granular levels of control can be provided for specific sections of the stack. Harnessing the multiple layers holistically under the cloud will facilitate the deployment of a single CBDC system. Autonomy and segregated control can be provided in a single system without a single party dominating the system.

Encrypting the data with maturing techniques such as homomorphic encryption (performing mathematical operations on obscured data) will also prevent service providers from tampering with it. The platform and its applications can be owned cooperatively by central banks, which have private keys and can continue to issue CBDCs.

Conclusion:

The next stage of the mBridge project will involve testing transactions with two stock exchanges in Hong Kong and Bangkok and thirty banks in four jurisdictions (i.e., Thailand, Hong Kong, China, and UAE). It will involve adding modular solutions to support liquidity allocation, competitive foreign exchange, compliance, and regulatory oversight. Transactional gridlock, in which transactions are mutually awaiting each other to settle will also need to be resolved.

With several other mCBDC projects (such as Project Dunbar and Project Jura) being underway, central banks will continue to test different governance models and methods for interfacing.

In the absence of blockchain, the prevailing correspondent banking model relies on financial intermediaries to facilitate cross-border transactions within a highly fragmented market. With its limited transparency, high compliance costs and lack of automation, this model of banking will likely continue its decline as mCBDCs are introduced as a new payment rail.

Thanks for reading! If you liked this post from FinS Soup for the Soul, why not share it? Have an awesome week ahead!